Taking Inventory

by John Hill

In response to historic inflation sponsored by unchecked COVID transfer payments, the Federal Reserve Bank initiated policy in March 2022 to bring inflation under control. A visible component of this policy – especially to anyone involved in real estate – is increased interest rates. Mothballed phrases like “buying points” – unuttered since prime rates dropped and stayed at 3.25% throughout most of the last decade – are back in vogue with real estate agents trying to ink deals on listings with growing housing inventory [1].

Since the government embarked on interest rate increases, Abilene inventory has mirrored national trends in its expansion. On the day prior to the quarter-point prime rate increase on March 17, 2022, Abilene housing inventory stood at 2.08 months worth of stock. Subsequent to this year’s five rate increases, housing inventory climbed throughout 2022, doubling that figure with a little more than 4 months of inventory in October 2022 [2].

So… 4 months of inventory and climbing with more interest rate increases likely to come. Not to get mired in the present, I looked at historical data on housing inventory to lend long-run context:

- First, a definition of a neutral housing market. By neutral market, I mean a level of housing inventory that gives neither a seller nor buyer the upper hand. The Texas Real Estate Center at Texas A&M offers 6.5 months as neutral inventory.

- In Abilene, we have to go back to 2014 to see inventory above 6.5 months and, even then, +6.5 months of inventory only occurred in January – a time in the calendar following the holidays acknowledged as a slow time for real estate transactions. These periods of neutral inventory were short-lived and inventory quickly returned to a position that benefitted sellers. Unlike current conditions, those blips took place during a prolonged period of 2% inflation and prime rates at 3.25%.

- Following 2014, a recovered economy with predictable 2% inflation gave the government the green light to raise rates, ultimately, to 5.5%. A rate reversal was initiated in July 2019 and the following January saw inventory momentarily climb above the winter spike realized in 2018 and 2017 under these higher interest rates.

- COVID hit, people sheltered in place and were afraid to put their homes on the market or look for a house, inventory climbed to 3.92 months in June 2020, the prime rate was cut to 3.25%, and PPP money was mainlined into the economy. The result: as we learned to live with pandemic conditions, we saw sub-2 month inventory occur 50 times between January 2021 to March 2022 and we experienced the most persistent seller’s market seen in years.

Two graphs frame this story. The first graph depicts the number of closing over 30 days and a 30-day average of total inventory. With each gain in inventory, we see an uptick in sales in all cases except one: the present. Before closings peaked at 223 on 7/30/2022 (three days after the interest rate hike on 7/27/2022), closings moved in tandem with inventory. After that, inventory and closings diverge, leading up to the current period with growing inventory figures.

The second graph shows the prime rate [3] and ratio of the two statistics in the first graph to calculate monthly inventory – again, this is total inventory divided by a month’s tally of closings. This graph illustrates the three periods of Abilene, single-family home sales addressed in the bullet points. It visualizes the secular, annual swings of inventory during flat, low rates prior to 2015, dampened inventory swings once rate increases begin in 2015, rates plummeting with COVID in 2020, and a supercharged market with low rates & PPP money that kept inventories low until the stimulus money ran out, loan deferrments sunsetted, and rates begin to climb.

Historical data shows four (and more) months of inventory is nothing new to buyers over the last decade, but this is the first time in many years that we’ve seen rising inventory in tandem with rising rates and rising inflation. Over the past two years, transactions were simple and had only a few moving parts – sellers expected they could price high and buyers knew they would have to fight to pay these higher prices. Changing inventory is changing how sellers (and real estate agents) will have to price to appeal to buyers.

As a broker, this caused me to give a hard look at the role of inventory on price. I need to understand how to price so I can provide value to sellers and help buyers negotiate better deals in the current economic climate.

To gauge the impact of inventory on pricing, I looked at Abilene sales dating back to January 1, 2010 – a total of 18,464 completed transactions [4]. Because these figures took place across time, I had to adjust price and other dollarized records using a price deflator to bring past sales into current or real terms [5]. Inventory was the primary variable I wanted to translate into sold price, but other factors have bearing on the price of a single-family home sale. To capture those other factors I considered:

- Square footage – larger homes, bigger price.

- Age of home at date of sale – the older the home, the lower the value of the home.

- Age of home at date of sale (squared) – this polynomial transformation measures gentrification. True, older homes lose value, but as they age, trees get bigger, neighborhoods become more established, and values increase.

- Unexempt property taxes – A problem with age, especially old age, is that it fails to measure a home’s condition – you can have two homes of the same age where one is old and decrepit, and the other is old and well-maintained. Using unexempt taxes presumes that an agent of the tax office lays eyes on each property and judges its condition on a spectrum from excellent to poor. This allows unexempt taxes to serve as a proxy for quality.

- Lot size (measured in acres) – the larger the lot size, the larger the value.

- Pool (Y / N) – a swimming pool adds value.

- Number of stories – a second floor decreases value, a third even more so. People in Abilene don’t like to climb stairs.

- Wylie ISD – Wylie ISD adds value relative to Abilene ISD.

- Mandatory HOA – an HOA is an additional agent that maintains quality of a neighborhood and adds value.

- Half baths – a half bath is a proxy for higher-end construction and adds value.

- Number of garage stalls – this adds value as people appreciate protection afforded by an enclosed garage. This is not the same thing as carport parking.

- No HVAC – no HVAC suggests a total gut job and subtracts value.

- Flooring – luxury vinyl plank (LVP) indicates the home owner updated their home. Wood floors are timeless and what LVP hopes to be (even though LVP helps the house sell for more than wood). Carpet suggests stains, odors, and an outdated home, negatively impacting price.

- Ratio of bedrooms to baths – it’s redundant to add bedrooms and baths once living area is accounted in the model. Instead, a ratio of bedrooms to bath is used to develop price. Think about which home you’d prefer: one with 3 bedrooms and 2 baths or 3 bedrooms and 1 bath – the former is preferrable because its easier for a family to get ready for work and school with the extra bath.

- Ratio of total living area to number of bedrooms – The book Freakonomics calls out the initially counterintuive and predictive word “spacious” when determining a home’s value. This euphemism slyly masks the real burden of worthless, poorly-designed square footage that you have to heat, cool, and maintain. The negative impact of spaciousness is measured by looking at a ratio of total square footage to private spaces.

- Number of months of inventory (squared) – my assumption is more inventory causes prices to fall at an increasing rate.

A linear regression model explaining sold price was performed that considered each of these factors [6]. The model estimates the parameter on month’s inventory squared as -$2403. Again, as months of inventory grow, this parameter suggests that prices decrease at an increasing rate. The table below makes that calculation, ceteris paribus:

| 1 month inventory | 2 months inventory | 3 months inventory | 4 months inventory | 5 months inventory | 6 months inventory | 7 months inventory | 8 months inventory | |

| impact to price | -$2,403 | -$9,612 | -$21,627 | -$38,448 | -$60,075 | -$86,508 | -$117,747 | -$153,792 | change by inventory | -$2,403 | -$7,209 | -$12,015 | -$16,821 | -$21,627 | -$26,433 | -$31,239 | -$36,045 |

Applying the model to the current year we can see the impact of inventory on prices. In January 1, 2022 we 2.08 month’s housing stock. By mid-October 2022 we had 4.3 months inventory. The outcome: a $34,035 drop in price [7], other factors held constant. If today’s inventory increases to the level of neutral inventory at 6.5 months, this model estimates an additional $57,000 adjustment to price. I’m not sure if this offers any comfort to sellers with homes on the market, but we aren’t there – yet.

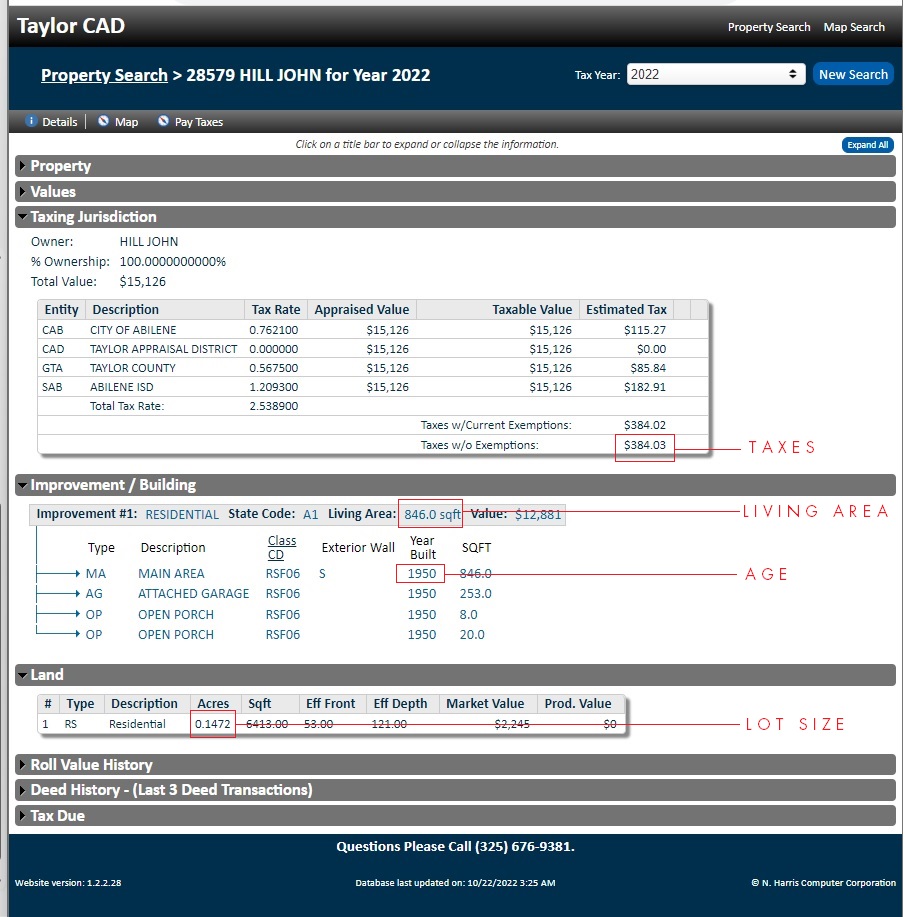

Curious how these current market conditions have affected the value of your Abilene-area home? The pricing tool featured below translates your home’s attributes and current inventory into an estimate of price. To use it accurately, you’ll need to perform a little leg work and search your property record on the Taylor Central Appraisal District website to get your 1) unexempt property taxes, 2) living area, 3) age, and the 4) lot size of your home. Once you’ve entered the information for your home, you can noodle with the inventory date to adjust months of inventory and make tangible the angst that you didn’t take advantage of 2021’s robust market conditions.

Obtaining your Taylor CAD data to estimate your home’s value ExpandUse this link to your Taylor CAD tax record to search for your property by its address. Once you’ve found it, you need 4 things from your online Taylor CAD record to estimate the value of your home:

- unexempt taxes

- living area

- age

- lot size

Once you’ve found your property record here are the 4 elements you need:

A final caveat: this tool is a good first pass at value, but it may not be YOUR value. Understand that each house is unique, not all the factors that drive value on a house are captured by this model. You need a real estate agent to assess the qualities of your home in the context of today’s market conditions to monetize these differences when you buy or sell.

Ready to sell? Call a Barnett & Hill agent to begin pricing your home to get it sold. Ready to buy? Call a Barnett & Hill agent who can leverage data like this to help you fight for the best price on your new home.

[1] The number of homes that are actively on the market divided by the number of homes that sold in the last month is the formal measure of inventory. For example, if 400 homes are on the market and 100 homes sold in the last 30 days, inventory is 4 months. This statistic suggests if consumers take down 100 homes per month, there are enough homes on market to sustain 4 months of purchasing.

[2] Typically inventory measures are summarized each month, yielding 12 snapshots per year on inventory. In this market where inventory is responding to changes in interest rates, 13 years of data was downloaded from NTREIS to develop a daily measure of inventory. This measure is based on a 30-day average of active, active-option, active-contingent, and pending listings divided by a total of closed sales over the same 30-day period.

[3] Federal Reserve Bank of St. Louis, Bank prime loan rate , https://fred.stlouisfed.org/series/DPRIME

[4] North Texas Real Estate Information System, proprietary data at https://ntreis.net/

[5] Federal Reserve Bank of St. Louis, Consumer Price Index for All Urban Consumers: All Items in U.S. City Average, https://fred.stlouisfed.org/series/CPIAUCSL

[6] This model had an adjusted R-squared of 82.3%. All independent terms were significant at the 99% level of confidence.

[7] $2,403*2.08*2.08-$2,403*4.3*4.3 = $10,396.34 – $44,431.47 = -$34,035.13